How to Use Credit Cards Wisely

The estimated reading time for this post is 177 seconds

Lenders want you to be creditworthy before they can finance that house, car, or new business, and the FICO credit score is how 90% of them determine that creditworthiness. Credit cards, secured or unsecured, are among the best ways to build a good credit score.

FICO Score

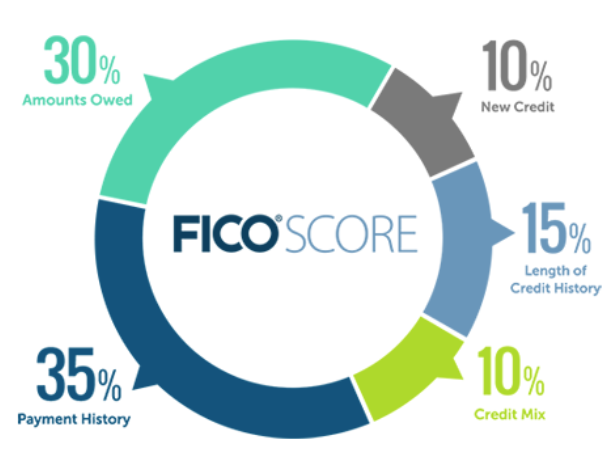

FICO credit score is a three-digit number based on information in your credit reports. Your mortgage, credit card, and auto loan payments, and other lending products tradelines in your credit reports.

Rental payments, utility bills, and many other consumer non-discretionary accounts are not in your reports. Equifax and Transunion are the three major credit agencies that compile information and maintain individual credit reports.

What’s in Your FICO Scores

Use Credit Cards Wisely

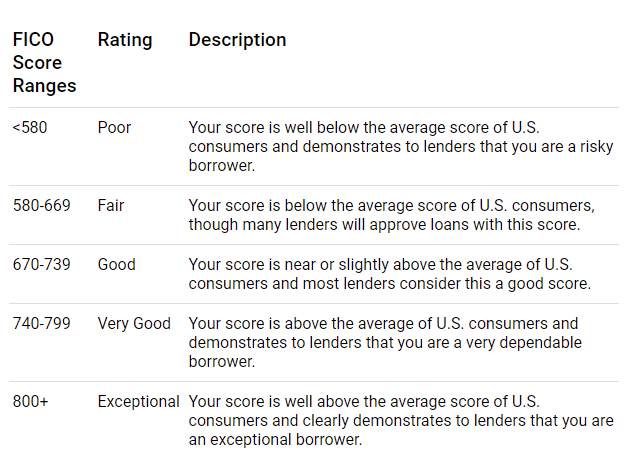

What Is a Good FICO Score

Pay Cash for Everything

Many personal finance advisors and coaches recommend their clients ditch out credit cards and pay cash for everything because they believe that all cash transactions will reduce frivolous spending.

That belief is half-true. Credit card users who take time to work on a personal finance budget take control of their finances. They only swipe their credit cards for budgeted nondiscretionary expenses.

Paying cash for significant financial transactions such as a home, car, and other big-ticket items is not something that most low and middle-income Americans can afford to do.

So, building an excellent credit profile has to be part of each American holistic financial planning. In this era of financial technology (Fintech), paying cash for everything can be a significant financial mistake.

The Dangers of Credit Cards

Use Credit Cards Wisely

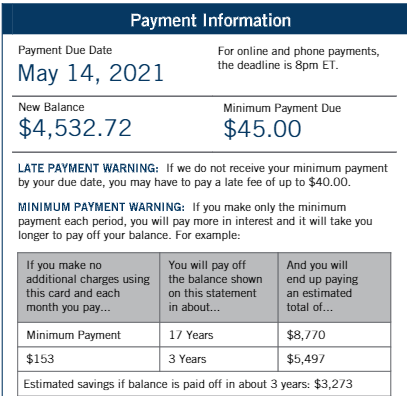

Without a solid budget, credit card users will overspend, and those who opt in to pay the minimum payment can find themselves in debt for decades.

Based on the above screenshot, it will take a credit user nearly 20 years to pay off her credit card balance of $4,532.72, resulting in $8,770 worth of interest expense with a 12.99 annual percentage rate (APR)

If the credit card user continues to use the card, the interest expense will be higher, and the pay-off date will be longer.

How to Use Credit Cards Wisely

Use Credit Cards Wisely

You can reduce or eliminate the interest expense if you use credit cards wisely. Credit card issuers love users who maintain an outstanding balance, continue to swipe and make the minimum monthly payment.

Pay Your Balance in Full Each Month

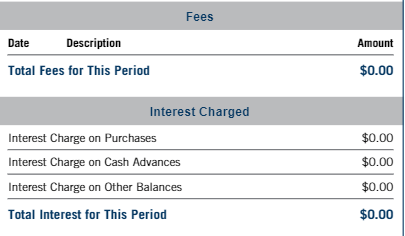

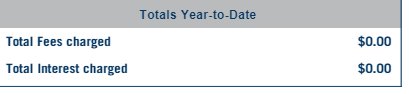

If you pay your credit card balance in full every month, you pay a $0.00 interest charge on purchases.

So instead of paying cash for everything, you can work on a personal finance budget and put all your non-discretionary expenses on a credit card and pay that balance in full on or before the payment due date each month.

Use Credit Cards Wisely

If you pay the balance in full each month, your total fees and interest charges should be $0.00 by year-end.

A little-known fact about paying your credit card in full each month, it’s a form of a short-term interest-free loan.

Conclusion

Credit cards are an expensive and dangerous product. However, if you learn how to use them wisely, you can build an excellent personal credit profile and have a perfect FICO score, which is how 90% of them determine creditworthiness.

You need to work on a personal budget to itemize your non-discretionary expenses, put those expenses on a credit card, and pay that card balance in full each month.

Pingback: Wells Fargo to Pull Customers Personal Lines of Credit - FMC

Pingback: Apple Card 2nd Year Anniversary: Should You Get It Now - FMC