Investing in the stock market is often seen as a pathway to building wealth and is one of the main ways Americans accumulate assets. However, when it comes to stock market participation, there is a significant gap between Black and White households.

According to a report by the Federal Reserve of St. Louis, the gap in stock market participation between Black and White households is large and persistent.

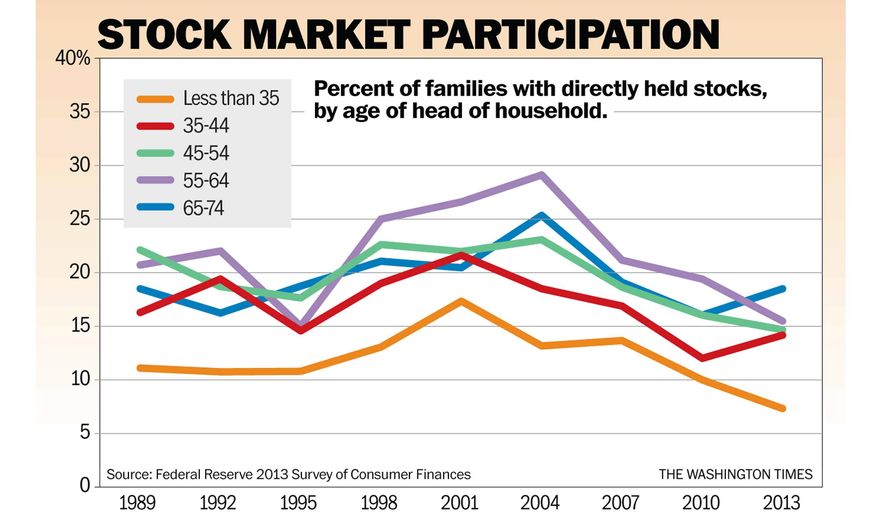

The report found that in 2019, 60% of White households held stocks directly or indirectly, compared to only 33% of Black households. This gap is even wider when it comes to direct stock ownership, with 55% of White households owning stocks directly compared to just 14% of Black households.

The report also found that this gap has persisted over time, with little improvement in stock market participation among Black households since the 1980s.

There are several reasons why this gap exists. One of the main factors is the wealth gap between Black and White households. According to the Federal Reserve of St. Louis, the median net worth of Black households in 2019 was just $24,100, compared to $188,200 for White households. This wealth gap means Black households have less money to invest in the stock market.

Another factor contributing to the gap in stock market participation is differences in education and financial literacy. Research has shown that people with higher education and financial literacy levels are more likely to invest in the stock market.

However, Black households are more likely to have lower education and financial literacy levels than White households. This makes it more difficult for Black households to understand the benefits of investing in the stock market and navigate the financial system’s complexities.

Furthermore, discrimination and historical factors also contribute to the gap. For example, historical discrimination in the housing market has led to Black households having less home equity, often used as collateral to secure loans for investing in the stock market.

Additionally, Black households are less likely to have access to financial advisors and other resources that can help them navigate the stock market.

Closing the gap in stock market participation between Black and White households will require a multifaceted approach.

One important step is to address the underlying causes of the wealth gap between Black and White households, such as discrimination in the housing market and access to quality education.

Improving financial literacy and education can also help reduce the gap in stock market participation and increase access to financial advisors and resources.

The large gap in stock market participation between Black and White households is a complex issue that requires attention from policymakers, financial institutions, and society.

By addressing the underlying causes of the gap, we can help create a more equitable and inclusive financial system for all Americans.

One way to increase stock market participation among Black households is through targeted education and outreach. Financial institutions can play a role in this by providing resources and education on investing in the stock market that are tailored to the needs of Black households.

This can include offering financial literacy programs and workshops addressing the unique challenges Black households face.

Another approach is to increase access to financial services and products for Black households. This includes providing affordable banking services and credit to underserved communities and expanding access to investment opportunities such as 401(k) plans and individual retirement accounts (IRAs).

By increasing access to financial services and products, more Black households may be able to invest in the stock market and build wealth over time.

Policymakers can also play a role in addressing the gap in stock market participation. For example, policies that address discrimination in the housing market and improve access to education can help to reduce the wealth gap between Black and White households.

Policies that promote financial education and literacy can also help to increase stock market participation among Black households.

In addition to these policy and institutional changes, there are also individual steps that Black households can take to increase their stock market participation. This includes seeking financial education and advice, using online resources to research investment opportunities, and starting small by investing in low-cost index funds.

In conclusion, the large gap in stock market participation between Black and White households is a complex issue requiring various stakeholders’ attention.

Addressing the underlying causes of the gap, including discrimination and historical factors, improving financial literacy, and increasing access to financial services and products can help to reduce the gap and create a more inclusive financial system.

By working together to address this issue, we can help to ensure that all Americans have access to the benefits of investing in the stock market and building wealth over time.