How to Avoid Paying Interest on Credit Cards

The estimated reading time for this post is 142 seconds

Avoid paying interest on credit cards can help build an emergency fund and strengthen your financial statement. We are not talking about free lunch here. After all, all loans carry interest charges.

Credit cards are the worst-best financial product–they give you great convenience and security, and they can ruin your finances and push you towards bankruptcy. So, how you navigate that thin line between financial security and financial disaster is imperative.

Credit Debt Is Expensive

Credit card issuers charge you an annual percentage rate (APR) for using their card. The APR can be between 15% and 29.99 percent. Credit card debt is expensive, and it can ruin your finances.

For example, if your credit company charges 27.74% APR* and your outstanding balance is $9,333, which is the average credit debt American consumer has, it will take you 14.5 years to pay it off if you don’t make any additional purchases.

By making a monthly payment of roughly $220, you will end up paying $28,655 worth of interest alone. Learn how interest rate works here

How Do You Avoid Paying Interest?

All you need to do is pay off the last statement balance in full by the due date. Let me explain–credit card companies, all of them, give you 25 days to pay your last statement balance. The twenty days is your grace period; as long as you pay that previous statement balance on or before the due date, you incur no finance charges

Here’s How It Works

If your statement closing date were on the 17th of December, the credit card company would give you until about the 15th of January to pay that last statement balance in full with no interest accrued.

Also, you pay no financing charges on all transactions made from December 18th through January 17th until February 15th. If you follow that formula, you have a lifetime 0.00% APR. You might get money from the credit card companies if you use a cash reward card.

Common Mistakes

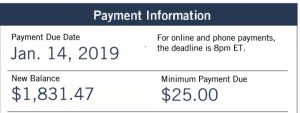

As you can see from the above screenshot, the payment due date is January 14th, and the minimum payment due is $25. If you make the minimum payment on January 14th, your account is in good standing with the credit card company. However, paying the minimum payment is the absolute wrong thing to do since the remaining balance from the last statement is going to be added to your new purchases to calculate interest charges.

Let’s say you pay the $25 on January 14th and go back and pay $1,806.47 ($1,831.47-$25.00) on January 18th, all your transactions from December 18th until January closing statement will accrue interest.

To avoid a finance charge, you have to pay all of the $1,831.47 on or before January 14, 2019.

When used correctly, credit cards can be an enhancement to one’s financial statement

*The Wells Fargo Cash Wise credit card charges APR up to 27.74%

Financial Nihilism: How Millennials and Gen Z Are Betting Against Economic Reality

Saving vs. Investing: What’s the Difference?